Asian steel markets may extend their tepid run into the July-September quarter, with participants keeping a close watch on the evolving US tariff situation and as key consuming centers enter a seasonal lull during summer and the monsoon.

While market sentiment improved slightly following measures to restrain steel output in the Chinese production hub of Tangshan and Shanxi province early in Q3, there were few signs that implementation would be forceful enough to address the imbalance between supply and demand.

Asian HRC, slab pressured by Chinese exports

Asian hot-rolled coil prices are likely to remain rangebound in Q3, according to market participants, amid oversupply pressures and flagging mill margins.

With mounting trade barriers targeting Chinese HRC exports, particularly from Vietnam and South Korea, Chinese steelmakers turned to South America and the Middle East. Still, overall volumes retreated 17% from a year ago to 12.1 million mt over January-May, according to China customs.

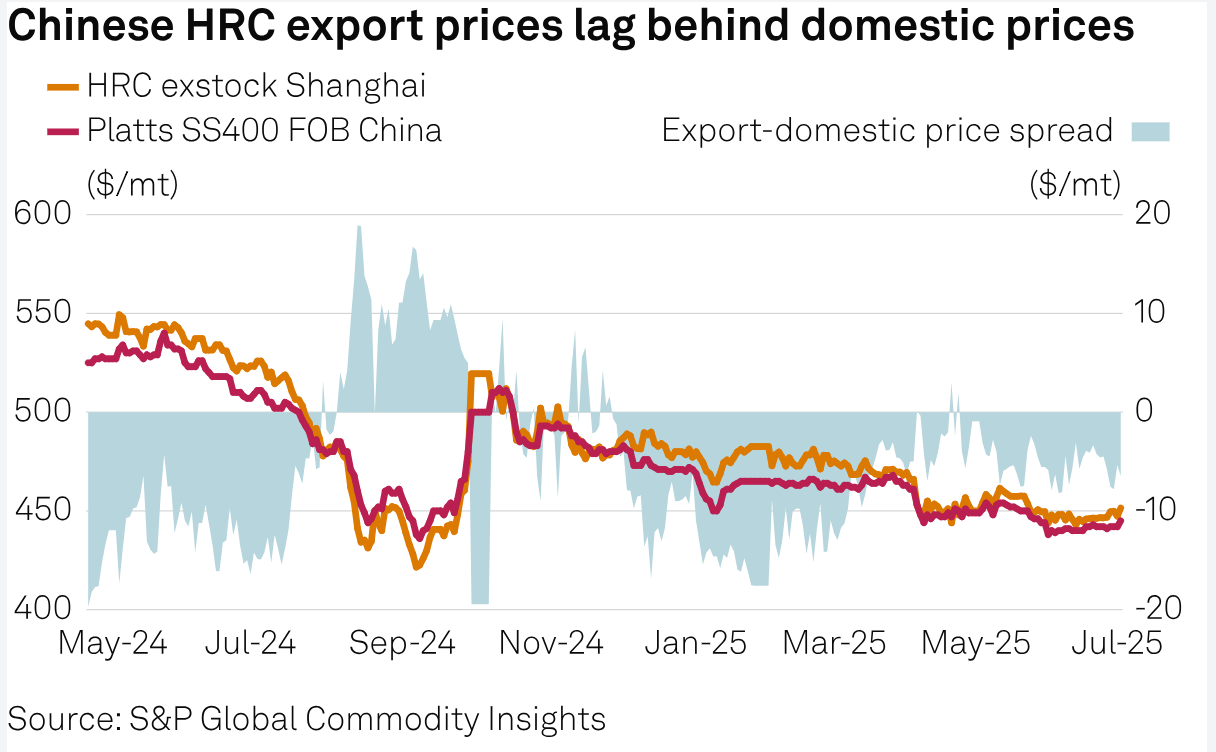

Besides volumes, export prices have also been under pressure. The spread between Chinese export and domestic HRC prices turned positive at the end of March, only to slip back into the negative territory entering Q2, suggesting that selling domestically would be more economically viable.

Meanwhile, the weak sentiment in the HRC market also pressured upstream slab prices.

On a CFR Southeast Asia basis, the spread between HRC and slab widened through the year so far, from $36/mt in March to $44/mt by June. Notably, the spread has widened over the past two years, from the low of a negative $20/mt in February 2024, according to Platts assessments by S&P Global Commodity Insights.

Moreover, many countries, including China and Japan, became more active in offering slab amid the slow offtake of HRC.

The number of spot seaborne trades, bids, offers, and indications for Chinese and Japanese slab on a CFR Southeast Asia basis surged to 14 in Q2, up from just 4 in Q1, data compiled by Platts showed.

Chinese billet exports seen staying elevated

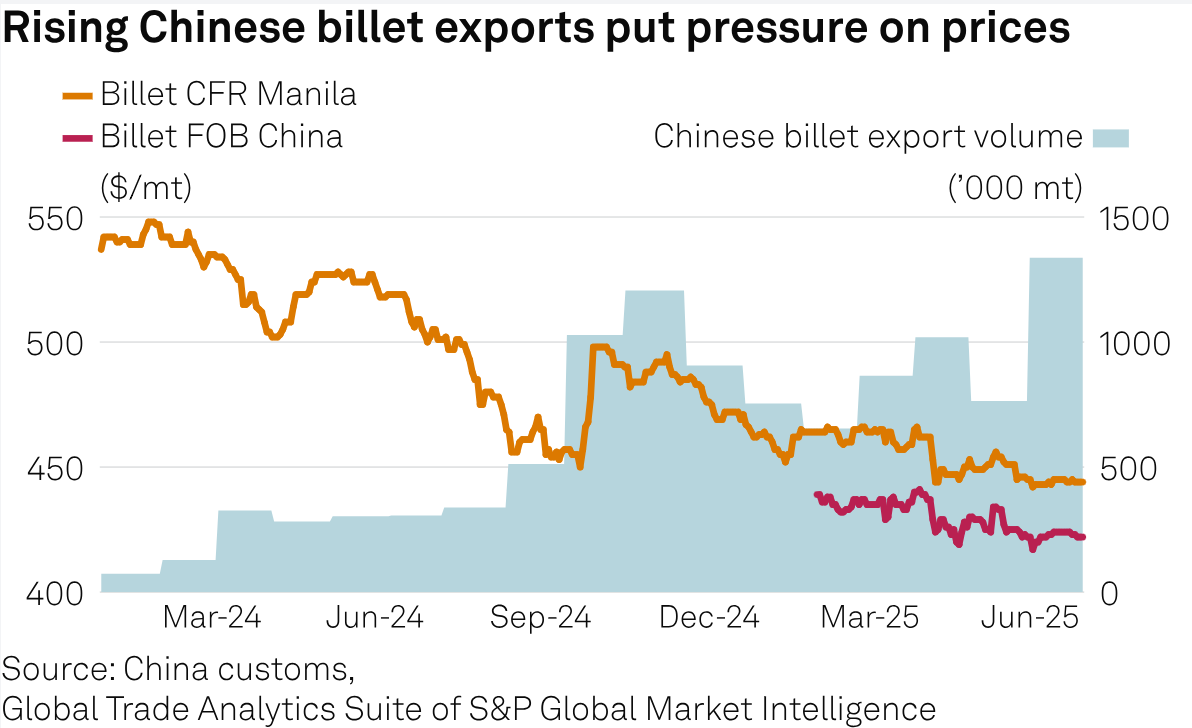

Asian billet prices will likely be under pressure in Q3 due to surging Chinese export volumes.

In Q2, Platts assessed 5SP 130 mm CFR Manila billet prices down 3% quarter over quarter at $448/mt, compared with a 6% decline in the previous quarter. While the downward trend extended into Q2, the extent of the decline eased due to support from rangebound raw material prices.

This trend came against a rapid growth in Chinese billet exports. Total exports from January to May totaled 2.64 million mt, almost eight times the volume over the same period in 2024, according to China customs.

The spread between rebar and billet on FOB China narrowed to $22/mt in Q2, from $27-$33/mt in early 2025, according to Platts data. The spread has also come closer to the processing cost of $20-$25/mt for turning billet in China, further spurring mills’ interest in exporting billet instead of rebar.

The rise in China’s semi-finished steel exports has drawn the attention of Chinese authorities, but market participants believe it would be challenging to implement effective curbs.

“The steelmakers [in China] are all struggling for survival. If there is any policy to refrain from exporting semis, domestic steel prices would plummet,” a mainstream Chinese mill source said.

China removed a 10% export duty on billet in January 2019. The annual export volumes of billet have been rising over the last few years, surging to 3.29 million mt in 2024 from 31,340 mt in 2021, according to China customs, amid the headwinds in the domestic property sector.

While HRC export volumes dropped, the surge in billet exports relieved supply pressure to some extent.

“China’s high finished steel exports have lasted longer than anticipated, marking an 8.5% year over year growth over the January-May period,” said Paul Bartholomew, senior analyst for metals and mining at Commodity Insights. “Exports will continue to act as a supply pressure relief valve. We estimate that China’s domestic steel consumption will fall by 2% on the year, while crude steel production so far is 1.7% lower on the year. Also, China has 182 million mt/year new capacity slated to come online over 2025-2026.”

Other than exports, market participants were wary that price upticks in the Chinese domestic market could not be achieved without an improvement in demand.

“A sustainable price increase cannot rely solely on the supply [cuts]. Even if production control measures in China are enforced, prices will continue to face downward pressure when the market recognizes the potential for unused capacity,” a Singapore-based trader said.

Although there are signs of easing trade tensions between the US and China, uncertainties linger before the final announcement and enforcement of US reciprocal tariffs, which is expected in August.

Billet supply pressures Asian scrap prices

The supply of billet has also impacted Asian ferrous scrap markets, even as prices of ferrous scrap in the US, the world’s largest exporter, stabilized after the country placed a 50% tariff on steel imports on May 30.

Asian scrap prices declined in Q2 amid competitive billet values and high production costs. Platts containerized HMS 1/2 80:20 CFR Unv1 index eased to $294/mt June 30 from a high of $319/mt March 13.

The surge in summer electricity rates in Unv1 from June has prompted electric-arc-furnace-based steelmakers to favor the purchase of billets over scrap.

In addition, the influx of billet imports, particularly from Russia and China, has intensified competition and lowered scrap prices in the region. The billet-scrap price spread fell to the year-to-date low of $133/mt on April 9 but stabilized around $150-$153/mt from June 13.