Asian steel markets may extend their tepid run into the July-September quarter, with participants keeping a close watch on the evolving US tariff situation and as key consuming centers enter a seasonal lull during summer and the monsoon. While market sentiment improved slightly following measures to restrain steel output in the Chinese production hub of Tangshan and Shanxi province early in Q3, there were few signs that implementation would be forceful enough to address the imbalance between

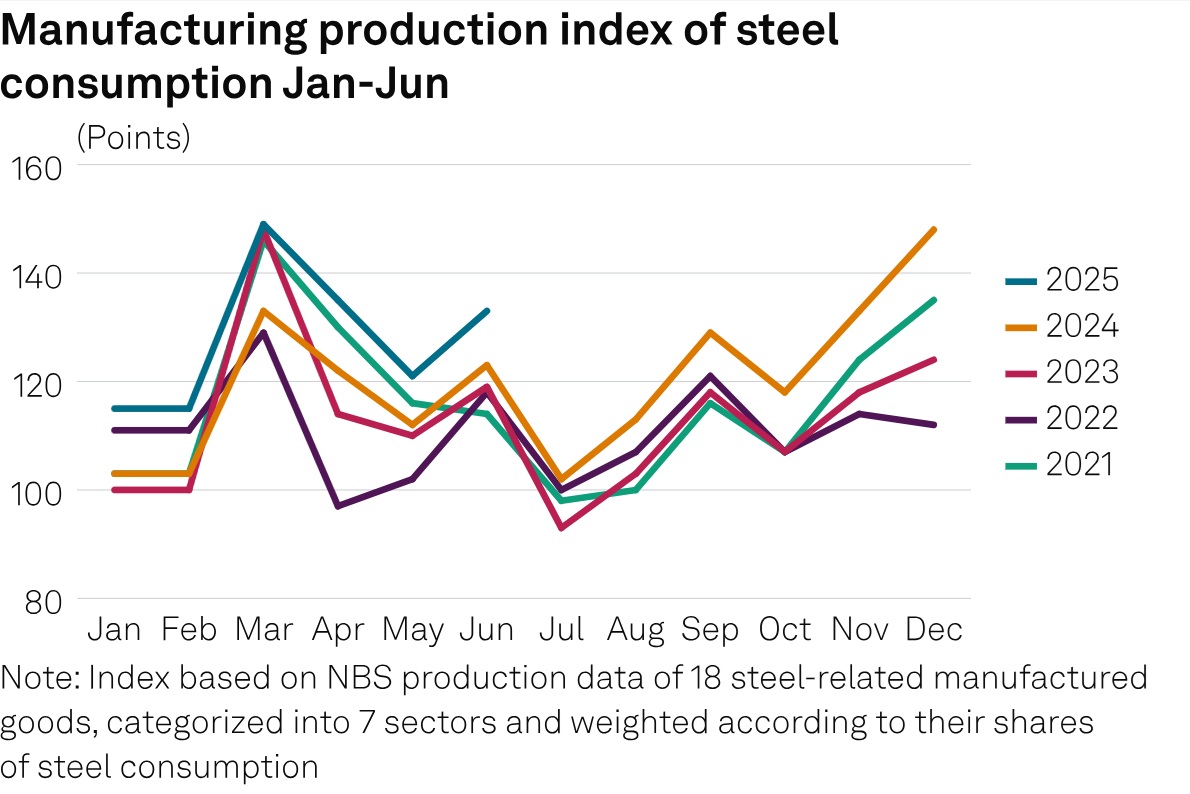

In June, the sectors of machineries, vehicles, home appliances, shipbuilding and power generation posted a year-on-year increase in production.

China’s Two Sessions held no real surprises for the commodity markets and hinted that the country faced an uphill battle to meet some of the critical energy, industrial and climate targets set under its 14th five-year plan (2021-2025).

Growing speculation over mandatory steel output cuts and capacity reductions in China may have boosted sentiment and steel prices lately, but market participants remain cautious over the outlook for the market.

更新中

Contact Us

fareast@fareaststeel.com

fareast@fareaststeel.com

+86 512 66516997

+86 13918196997

+86 512 66516997

+86 13918196997

16F, Tower C Suzhou Center Plaza, No. 217 Xinggang Street, Suzhou, 215021, China

16F, Tower C Suzhou Center Plaza, No. 217 Xinggang Street, Suzhou, 215021, China