QUOTE FROM PLATTS,

China’s manufacturing production in June continued to show robust year-over-year growth, led by solid exports and government subsidies that boosted domestic consumption.

However, China’s steel demand from the manufacturing sector is set to slow down in the second half of 2025, in tandem with relatively strong exports of Chinese manufactured goods, China-based market participants told S&P Global Commodity Insights.

That would mean both the factors would provide steady support to manufacturing production and related steel demand, they added.

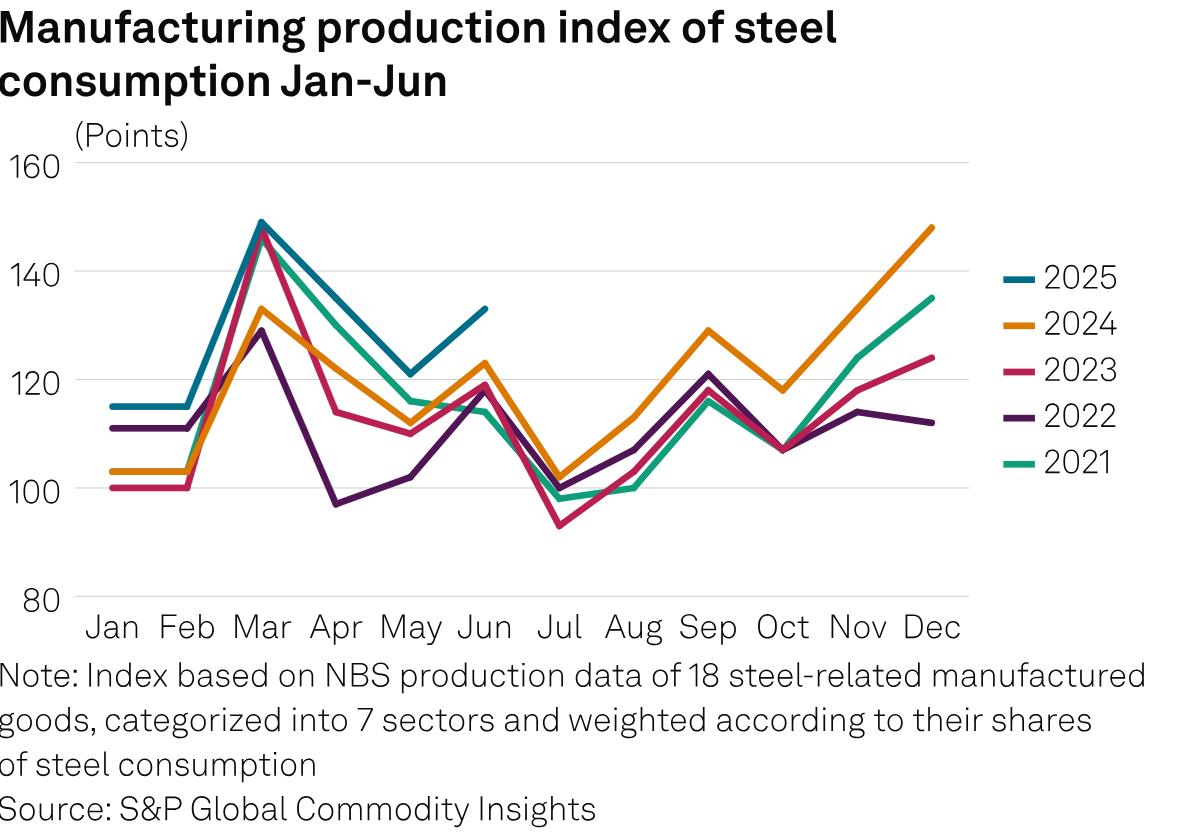

China’s manufacturing production index of steel consumption produced by Platts stood at 133 for June, up by 12 points from May and 10 points from the same period of 2024. Platts is part of S&P Global Commodity Insights.

The production index is based on production data from China's National Bureau of Statistics for 18 steel-intensive manufactured goods, categorized into seven sectors and weighted according to their share of steel consumption. The monthly production average in 2018 is used as the baseline of 100.

In June, the sectors of machineries, vehicles, home appliances, shipbuilding and power generation posted a year-on-year increase in production, while only containers and railway facilities posted a year-on-year decrease, according to the NBS data.

Strong exports

Robust exports remained a big contribution to the manufacturing sector’s good performance in June.

In June, China’s exports of mechanical and electrical products, a crucial source of growth for manufacturing steel demand, were 8.2% higher year over year in US dollar value, China’s customs data showed.

Mechanical and electrical products exports over January-June increased 8.2% on the year, accelerating from a 7.5% year-on-year growth in 2024.

China’s vehicle exports also remained strong in June, up by 27% on the year to 619,000 units.

“Due to strong overseas orders, Chinese shipbuilding companies have had their backlog of shipbuilding orders extended to 2028. Therefore, the steel demand from the shipbuilding industry has been robust so far this year, and the strength is expected to continue at least until 2027,” said a mill source.

“It’s within expectations that the growth of China’s manufactured goods exports could slow down in the second half of the year, as export rush in the first half, in a bid to avoid further escalation of the US tariffs, has brought some demand forward,” said a China-based market observer.

“But, overall, I think the exports of China’s manufactured goods can [remain] strong in a long run, due to the cost advantages brought about by the completeness of its manufacturing system.”

Concerns over domestic consumption

Another factor that is driving China’s manufacturing sector this year is government subsidies for domestic consumer goods trade-ins, which have boosted sales of steel-intensive manufactured goods, such as cars and home appliances, said some sources.

However, the proportion of subsidies in H2 could be lower than in the first half, they said.

China has allocated Yuan 162 billion ($22.59 billion) of ultra-long special treasury bonds for consumer goods trade-ins as of April, while the remaining quota of Yuan 138 billion will be distributed in the second half of 2025, according to the NBS.

China’s trade-in subsidies cannot create demand, but mainly have brought future demand forward, and that would mean growth in domestic consumer goods consumption may decelerate later this year, some steel market sources said.

“China’s manufacturing sector is unlikely to generate much incremental steel demand in the second half, but I don’t think the manufacturing steel demand would suddenly turn into a downward trend either, as export markets will remain resilient, and more policy stimulus will be introduced to at least ensure the stability of domestic consumption,” said another mill source.

HRC market

Due to the strong performance in manufacturing sector over the first half of 2025, China’s domestic hot-rolled coil sales profit margins, a proxy for flat steel market targeting mainly manufacturers, stayed quite stable for much of the first six months, at around Yuan 100-150/mt ($13.9-20.9/mt), despite higher HRC production.

China’s medium-thick HRC output over January-June increased 4.3% on the year to 114.01 million mt, according to the NBS.

Some market sources said the growth of manufacturing steel demand could lack momentum in the second half of 2025 and, as a result, HRC profit margins would be unlikely to improve in that case.

However, if steel mills can strictly carry out production cuts, Chinese steel mills in general could remain profitable for the rest 2025, said the sources.

Market talk indicated that China is set to reduce its crude steel output in 2025 by 50 million mt from the 2024 level. Over January-June, China’s crude steel output was down by 3%, or 15.92 million mt, on the year to 514.83 million mt, NBS data showed.